The state of ecommerce: Q3 2025

E-commerce sales showed remarkable resilience in Q3 2025, with Ordered Product Sales up 9% year-over-year despite economic headwinds. Growth was strongest in Grocery, Health & Personal Care, and Toys categories. However, this growth came with a cost—unit margins declined by 2-3% as brands absorbed rising input costs, implemented deeper Prime Day discounting and faced mounting tariff pressures.

Supply chains demonstrated stability with inventory levels increasing 19% year-over-year and Purchase Order fill rates improving to approximately 90%. Yet out-of-stock incidents continue to cause significant revenue losses, particularly in high-velocity categories like Grocery and Pet Products, highlighting the need for more sophisticated safety stock strategies and inventory management.

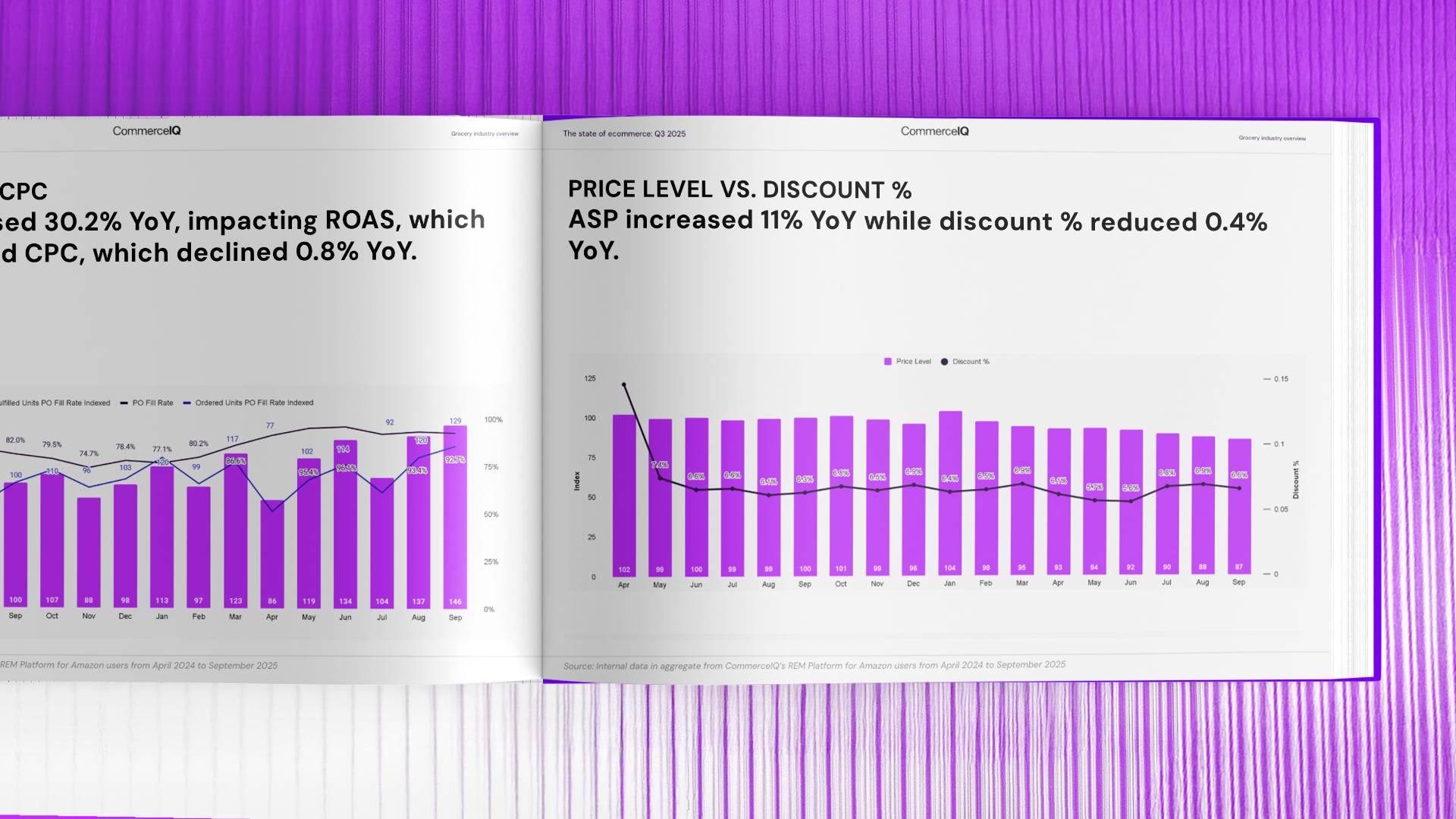

The advertising environment grew more competitive with retail media spending surging 22% year-over-year, while Cost Per Click and Return on Ad Spend remained relatively flat. This indicates brands are spending more to maintain visibility rather than gaining true efficiency. As Q3 closes, brands face a challenging balance: managing rising costs and competitive pressures while maintaining growth ahead of the crucial holiday quarter.

Download the full report

Used by the most loved brands in the world

Key takeaways

- Sales growth came at the cost of margin: Sales rose 9% YoY, but profits fell as brands relied on discounting and absorbed higher input costs

- Supply chains held firm: Inventory grew 19% and fill rates hit 90%, proving brands can meet demand despite cost & logistics pressure

- Out-of-stocks still drive significant revenue loss: Low OOS rates mask high revenue impact, particularly in Grocery & Pet categories

- Retail media spend outpaced returns: Ad spend jumped 22% YoY while CPC & ROAS stayed flat, showing more spend is needed to hold market share

- Shoppers shifted toward value: Traffic was flat but conversion rose slightly as consumers opted for lower-priced, smaller pack sizes

- Category performance was uneven: Grocery, Health & Personal Care, & Toys grew strongly, while Tools, Patio, & Furniture lagged